Douglas Morris of Emerson’s alternative energy industry team shares some thoughts and experiences from the CERAWeek conference this week.

The 32nd annual CERAWeek Conference, led by Daniel Yergin, was held this week in Houston, Texas USA. The meeting is the preeminent global energy get together and gathers leaders from the world of energy companies to discuss the latest trends and challenges. The theme of this year’s event was “Drivers of Change: Geopolitics, Markets, and the New Map of Energy.”

If I were to sum things up, the primary theme for this year was “unconventional energy.” As with last year, the far reaching impacts of shale gas was a prominent topic, but added to this was shale oil, tight oil, NGLs, and more. Each day of the conference is thematic with the goal of trying to connect the dots of the global energy value chain. Day one is about macroeconomic trends, day two is “oil day”, day three is all about gas, day four about power, and the final day is a look to the future.

Unconventional oil sources are combining to shake up the industry. For example, tight oil plays from the Bakken formation in North Dakota are helping to make the United States oil rich and, in combination with Canadian oil, North America will oil independent and will no longer need imports. Just about a half decade ago, the country was at its peak in imports and was looking at alternative fuels to help mitigate the need for imported oil. Oh how times have changed.

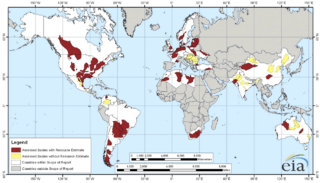

Shale gas continues to shake things up. At current rates, the production of shale gas in the United States puts it on pace to become the world’s largest gas producer. Remember when we were building regasification terminals a while back because of our need for gas? Now the discussion is how many LNG export facilities will be constructed. There are currently 16 proposed in the country, with one, Cheniere Energy already approved. The availability and forward looking price stability of gas is even impacting the rail industry where BNSF just announced that it will be piloting a change in fuels for its engines from diesel to LNG. It’s being described as an inflection point like when locomotives switched over from steam power.Source: Wikipedia – 48 Shale basins in 38 countries, as per the EIA

Gas is also affecting the power industry in that there are more and more gas plants being built to replace coal fired assets. Based on the price of gas, gas plants are now being dispatched ahead of coal for many utilities and their generation fleets are rebalancing to include more gas and fewer coal assets. This trend is likely permanent, although commercial utilities will always maintain a balanced mix of generation as a hedge to risk.

Always a fun experience and I look forward to seeing how these new unconventional resources continue to change the dynamic global energy industry.

It became very clear to me how shale gas is causing an inflection point in the industry on many different fronts, starting with the long-term cost curve of natural gas. With the huge supply of gas from shale, experts in the industry predict the price of gas to remain relatively inelastic far into the future. Just today, there was an article in the Wall Street Journal that discusses how cheap gas has become ($2.27 per 1,000 cubic feet as of today in New York trading). What a change from the 2000s where the price of gas on a chart looked more like a sine wave! There is so much gas that county has done a complete 180 on LNG. Just a few years ago, we were building LNG regas terminals to prepare for gas imports from Qatar. Now we have one export terminal approved with others lining up to gain approval to supply gas to the European and Asian LNG markets where gas trades at about $9 and $13 per 1,000 cubic feet respectively.